Content

Examples include short-term Investments, prepaid expenses, supplies, land, equipment, furniture & fixtures, discount income account, etc. are the type of temporary accounts covered under revenue and gains. Temporary accounts are accounts that are reset after a fixed period with respect to accounting. The resetting of these accounts is owing to calculating the gains or losses of the particular accounting period. Therefore, temporary account numbers are independent of the performance of the company in previous financial years. Temporary accounts allow financial managers to separately record, calculate, and analyze transactions that reflect on the business’s performance for a particular, defined period of time. Temporary accounts allow for greater accuracy in reporting this activity and feeding it into financial statements.

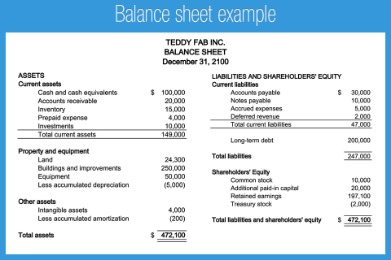

Business owners who can distinguish permanent and Temporary Accounts have an advantage when making wise business decisions since they have a better understanding of their company’s financials. Businesses may maximize their investments and make educated decisions with greater financial knowledge. You may also choose to create a temporaryincome summaryaccount, which helps with theend-of-the-year closing process. It’s where you combine all the other accounts and calculatenet profit—and transfer those funds to the right permanent accounts. The account balances for the permanent accounts such as Cash and Equipment will remain constant from the adjusted trial balance through the post-closing trial balance. At the end of each quarter, publicly traded companies need to organize their accounts and publish financial statements.

Benefits of Understanding Temporary and Permanent Accounts

Businesses can more precisely plan for the future when they are aware of the temporary and permanent accounts. This enables them to develop long-term goals based on accurate estimates as opposed to conjecture. As a result, companies may more confidently prepare for success. Accounts that are properly categorized help a corporation allocate resources more effectively to meet its goals. Understanding permanent and https://kelleysbookkeeping.com/ can help firms create budgets that accurately reflect their present condition and objectives. Whether saving for a short-term goal or planning for the future, there’s a temporary or permanent account that can meet your needs.

- The revenue account is used to keep track of all money earned during a given period of time.

- These transactions accumulate throughout the month or until the accounting period is over.

- A revenue account is a temporary account used to track the money a business receives in exchange for the goods and services it provides to customers.

- Temporary accounts are typically available only for 30 days or upon the student/instructor gets full access to Blackboard using their official UTRGV account.

- Instead, why not look at automating the entire process with the use of accounting software?

- This agreement usually lasts six months or longer and allows tenants to move elsewhere when their lease ends.

Permanent accounts start each accounting period with a zero balance. Revenue accounts serve as financial snapshots that provide a concise picture of how much money brought in and where these funds come from. This information lets businesses make more informed decisions on budgeting and investment strategies by giving them insight into estimated future earnings.

Retirement Accounts – Temporary Accounts

He is the sole author of all the materials on AccountingCoach.com. The Structured Query Language comprises several different data types that allow it to store different types of information… Closing the Income Summary account—transferring the balance of the Income Summary account to the Retained Earnings account. If you’re using TweetDeck and are locked out of your account, please sign out of and close TweetDeck entirely.

What are examples of temporary accounts?

- Earned interest.

- Sales discounts.

- Sales returns.

- Utilities.

- Rent.

- Other expenses.